On May 15, 2025, we poured a drink, and raised it to the ceiling. That roof? It’s officially ours. Paid in full. Not a penny owed. It took 2,120 days, a pandemic, some hard-core budgeting, and a lot of spreadsheets. But we did it — and I’m sharing the actual numbers so you can see what it really takes (and what it really costs).

The Purchase

We bought our home in July 2019 for $620,000.

We put $141,138 down — which was mainly the equity from selling my condo and helped to keep our monthly payments reasonable.

Our original loan was $484,350 at a 4% fixed rate for 30 years.

We hit the ground running and started throwing every extra dollar we had toward the mortgage. For the first several months, we were relentless. Side gigs, promotions, bonuses — anything extra went toward the house. Mr. Cabbage and I were on a mission.

Enter: COVID

When the pandemic hit in 2020, we panicked. Would we keep our jobs? Would our income change? We slowed down on the aggressive payments and got conservative. But here’s where the universe tossed us a curveball — in a good way.

Our lender reached out and said, “Hey, you should really refinance. Rates have dropped.”

The Refinance

In April 2020, we refinanced to a 20-year loan at 3.15%.

The refinance cost us $10,317 (ugh).

But the new principal? $416,250. That means we had already chipped away over $68,000 in just nine months.

Worth it? 100%. We were paying less interest overall, even with the fee.

The Finish Line

We made our final mortgage payment on May 15, 2025. That’s just under six years — 5 years, 9.5 months, to be precise — since we bought the house. That’s a 30-year mortgage annihilated in less than six.

Cue the champagne and confetti.

What It Cost Us

Let’s break it down:

- Purchase price: $620,000

- Down payment: $141,138

- Original loan: $484,350

- Refinance cost: $10,317

- Refinance loan amount (April 2020): $416,250

- Final payment date: May 15, 2025 (2,120 days purchase to payoff)

💸 Total interest paid: $79,611

💸 Total paid (principal + interest + loan origination + earnest money + refinance fees): $721,916

💸 Interest saved: $262,617

We didn’t do this because we’re rich. We did it because we hate debt. Because we treat interest like it’s setting our money on fire. Because Mr. Cabbage still remembers that closing agent smirking and saying, “Oh, you don’t have to look at that amortization schedule.” (He almost walked out and didn’t sign the mortgage. The amortization schedule is the only thing that matters.)

We did it by prioritizing. By skipping new cars and designer handbags. By putting our money toward freedom — and now, we have it.

Would We Do It Again?

Absolutely. Every extra payment gave us more equity, more breathing room, and more confidence. And now? No rent, no mortgage, no problem. And now, the kittens have all the security their tiny, murderous paws could want — they’ve been handling lizards and snakes like pros. I just wish they’d stop presenting their victims to me like little mafia enforcers.

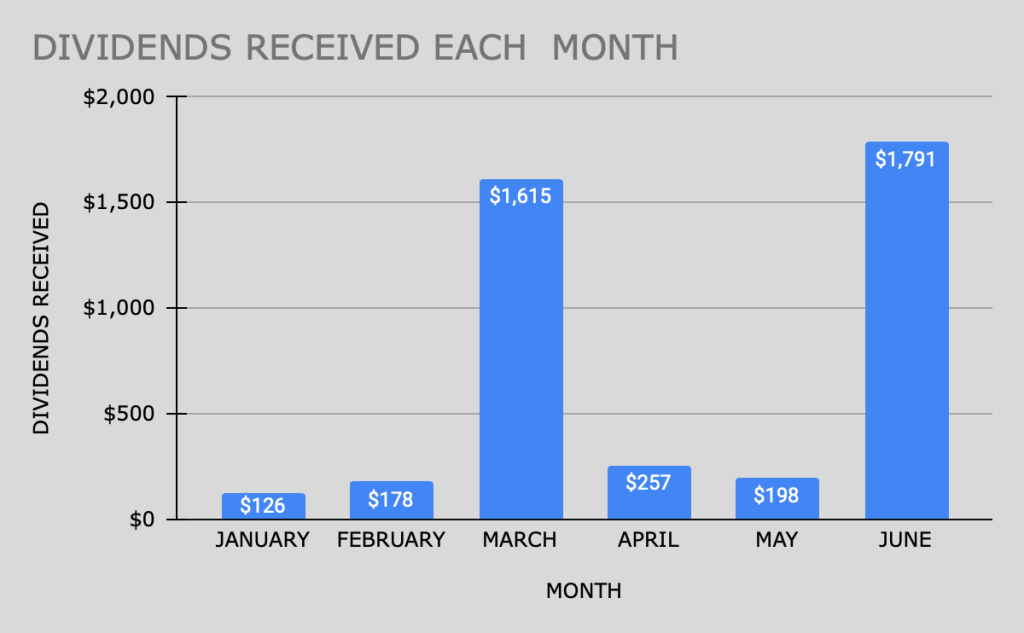

Stay tuned — I’ll share how we’re investing that freed-up cash next.

Because being debt-free isn’t the end. It’s only the beginning.

Tell me what you think!